The deal closed in two hours. That's the detail nobody is talking about loudly enough.

Nexstar Media Group received FCC and DOJ clearance for its $3.5 billion acquisition of Tegna on Thursday, March 19, 2026 — and the transaction was done within 120 minutes of that approval. Eight state attorneys general had already filed a federal antitrust lawsuit in Sacramento the previous evening. DirecTV had filed its own suit that same morning. None of it mattered. The merger was legally complete before any court could read an emergency brief.

That speed wasn't administrative efficiency. It was strategy. And it'll show up on your cable bill.

What Changed

Nexstar now controls 265 full-power television stations across 44 states, reaching between 60% and 80% of US TV households depending on whose accounting you use. The FCC approved this by waiving a decades-old rule capping any single broadcaster from reaching more than 39% of US TV households — approved through the Media Bureau in a closed session with no full Commission vote and no public hearing.

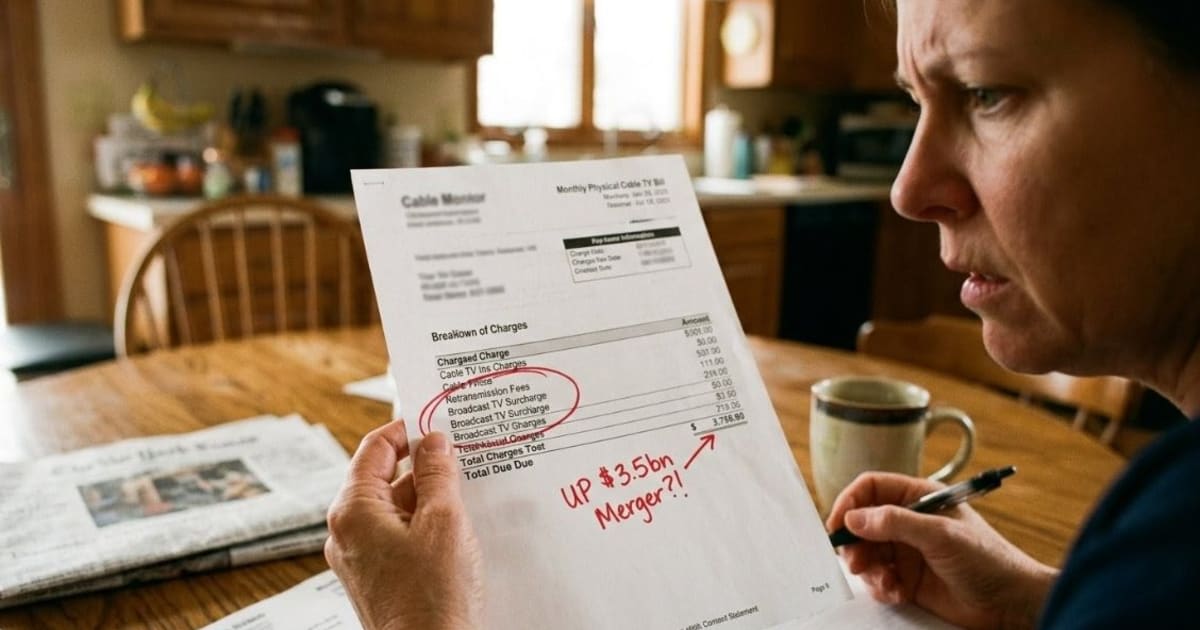

The mechanism that makes this a bill story rather than just a media story: retransmission consent. Under the 1992 Cable Television Consumer Protection Act, local broadcast stations can demand payment from cable and satellite companies to carry their over-the-air signals. Those fees are passed directly to subscribers as line items on your statement.

Nexstar's retransmission revenue trajectory:

- 2024: $2.9 billion — surpassing its entire advertising revenue

- Tegna's 2024 retransmission revenue: ~$800 million

- Combined entity's retransmission income: ~$3.7 billion/year

- Average retransmission fee per subscriber (2024): $22.62/month — up 14% in a single year per S&P Global Kagan

That's before Nexstar negotiates a single new contract with 265 stations rather than 201.

How Retransmission Fees Reach Your Wallet

The mechanism runs on one simple fact: there's no substitute.

- Nexstar owns your local ABC, NBC, CBS, or Fox affiliate in your market

- Comcast, DirecTV, or your streaming service must carry it on basic tier — it's legally required

- Nexstar sets the fee; distributors pay or face a blackout

- In 2019, Nexstar blacked out 120 stations across 97 markets in a retransmission dispute with DirecTV — about two weeks until a new fee was reached

- That threat now covers 265 stations across 132 markets

- Distributors understand this arithmetic before sitting down to negotiate

Who's exposed beyond traditional cable:

Virtual pay-TV services — YouTube TV, Hulu Live, DirecTV Stream — pay retransmission fees embedded in their monthly prices. A 10–15% increase in Nexstar's post-merger fee demands could add $3–5 to streaming live-TV subscriptions too, not just cable bundles.

How Much More You'll Pay

Nexstar committed to freeze retransmission rates through November 30, 2026 as a condition of FCC approval. After that date, negotiations begin with 265 stations.

What analysts expect from November 2026 onwards:

| What changes | Estimate | Source |

|---|---|---|

| Additional monthly cost per subscriber | $3–5/month | S&P Global Kagan analysts |

| Annual impact per household | $36–60 | At $3–5/month |

| UK equivalent | ~£28–47/year | At current exchange rates |

| Indian equivalent | ~₹3,000–5,000/year | At current rates |

| Comcast broadcast TV surcharge increase (Jan 2025 alone) | $4.75/month | Comcast Q1 2025 filing |

S&P Global Kagan projects industry-wide retransmission revenues to reach $15.93 billion by 2027, up from $14.8 billion currently. Nexstar, as the dominant player, captures a disproportionate share.

Eight states and DirecTV have filed suit in US District Court for the Eastern District of California. The states invoke Section 7 of the Clayton Act — that the merger substantially lessens competition. In 31 media markets, Nexstar and Tegna stations currently compete head-to-head. After merger, that competition disappears.

Nexstar's retransmission freeze is the only thing standing between subscribers and higher fees — and it expires in eight months.

What Your Cable Bill Looks Like After This

If the Sacramento court denies the emergency restraining order — the most likely near-term outcome, given courts are structurally reluctant to unwind legally closed transactions — integration proceeds and November 30, 2026 becomes the date that matters. After that date, your cable or streaming live-TV bill absorbs Nexstar's new negotiating position. For the average cable subscriber paying somewhere around $90–120/month on a mid-tier package, a $3–5 monthly increase starting in mid-2027 represents a 2.5–5.5% hike from a single broadcast ownership change — before any other price adjustment your provider makes. That's roughly $36–60 per year, every year, in perpetuity. The race Nexstar ran on March 19 successfully outpaced the courts. Whether you have cable or a streaming live-TV service, the retransmission fee that just got bigger is already inside your subscription.

This content is informational only and should not be interpreted as a recommendation to buy, sell, or hold any security. Seek professional financial advice before acting on anything you read here.